One of India’s best investment schemes, many government employees invest in this fund for safety purposes. This fund is government-backed. As people explore ways to invest in NPS (National Pension System), one common question pops up: How to invest a lump sum in NPS 2025

This article breaks it down in simple terms. Whether you’re just starting to look at pension options or you’re comparing NPS with other investment methods, we’ve got you covered. Let’s explore whether lump sum investment in nps is a smart move and even allowed.

Let’s keep it simple, like a heartfelt prayer. You want peace in your old age. You want your needs met, not just today, but 20 years from now. And that’s exactly why you’re here to understand how to build that peace through the NPS (National Pension System) and learn from two decades of my own experience with the NPS (National Pension System)

How to invest a lump sum in NPS

How to invest a lump sum in NPS 2025? Is it allowed?

Yes, you can invest a lump sum in NPS. Contrary to the myth that NPS only accepts systematic or monthly improvements, it allows for flexible investment, including one-time, large improvements.

The Tier I account requires a minimum of ₹500 per transaction and ₹1,000 per financial year. Beyond that, there’s no upper limit to how much you Can Invest in NPS lumpsum. You can choose to invest ₹10,000 or ₹10 lakhs in a single go; there are no restrictions unless specified under certain employer-employee schemes.

Understand the NPS (National Pension System).

NPS Tier 1 is like a lifelong friend that grows with you. It’s a retirement-focused investment backed by the Government of India. How to invest a lump sum in NPS regularly, monthly, or yearly and build a pension corpus? After 60, you can withdraw part of it, and the rest becomes your monthly pension.

Anyone under 65, looking for a long-term pension, especially if you’re salaried or self-employed and serious about saving tax.

The National Pension System (NPS) was made for a long-term investment retirement plan by the Fund Development Authority (PFRDA). It’s designed for those people, especially those in the unorganised sector, to save for retirement systematically. and need a Retirement plan through work

Key Features of NPS

- NPS Eligibility: Open to Indian citizens aged between 18 to 70 years.

- Account Types: Two types, Tier I (mandatory) and Tier II (optional). Tier I is the core retirement account with tax benefits, while Tier II offers more flexibility but fewer tax incentives.

- Investment Options: NPS allows you to choose from different asset classes: Equity (E), Corporate Debt (C), Government Bonds (G), and Alternative Investment Funds (A).

- Returns: Unlike PPF or EPF, returns aren’t fixed. They depend on market performance but have historically ranged between 8% to 10%. NPS calculator can you calculate your money in this tool easily

Benefits of Investing in NPS

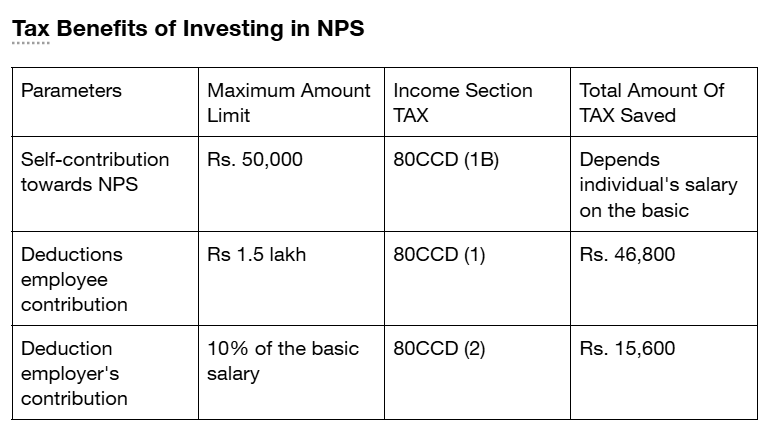

- Tax Benefits: up to ₹1.5 lakh qualify under Section 80CCD(1), and an additional ₹50,000 is deductible under Section 80CCD(1B).

- Low Management Fees: NPS has one of the lowest fund management charges in India.

- Professional Fund Management: Managed by top-notch fund managers approved by PFRDA.

- Flexible: No fixed frequency, you can contribute monthly, quarterly, or even yearly.

Advantages of Lump Sum Investment in NPS

- Convenience: one-time investment in nps effort. No need for multiple reminders or auto-debits.

- Market Timing: If you invest when the market is low, you stand to gain more as markets rise.

- Tax Planning: Helps you utilise the full ₹2 lakh deduction in one go.

Disadvantages of Lump Sum Investment in NPS

- Market Risk: Investing a large sum at once can expose you to immediate market volatility.

- Lock-in Period: Since Tier I has a lock-in until the age of 60, your lump sum is essentially illiquid until retirement.

- No Rupee-Cost Averaging: Unlike SIPs (Systematic Investment Plans), lump sum investments don’t smooth out market highs and lows.

Which Pension Fund Manager Is Best for NPS Tier 1 in 2025?

The Pension Fund Manager (PFM) is the shepherd of your retirement savings. And like a wise shepherd, they must lead your money through the ups and downs of the market.

2025 TOP PFMs STAND-OUT FUNDS

HDFC Pension Fund

- Returns: Top performer in equity and government bonds.

- Why choose: Aggressive yet balanced.

- Who it suits: Young investors (age below 45) who want growth over time.

SBI Pension Fund

- Returns: Consistent, stable performer.

- Why choose: The Trust of India’s largest bank.

- Who it suits: Those who prefer safety with moderate returns.

LIC Pension Fund

- Returns: Not the highest, but very stable.

- Why choose: Great for conservative investors.

- Who it suits: Older investors or those close to retirement.

Can you Invest Once a Year in NPS?

The rule is simple:

- Minimum yearly investment: ₹1,000

- Maximum? No limit. Can you invest a lump sum in NPS ₹5,000 or ₹5 lakh, your choice?

So, if you’re busy or want to invest once a year, say in March during the tax-saving season, you are free to do that. Small monthly investments grow stronger over a one-time investment in nps than one big drop at the end.

How Can You Get ₹50,000 Pension Per Month From NPS?

This is a question every wise investor asks. And the answer lies in planning backwards.

To get ₹50,000/month pension for life:

- You need ₹1.2 Crores at retirement.

- This means building that amount over 25-30 years through regular investing.

If you are 30 now and plan to retire at 60:

- Invest ₹10,000 per month (assuming a 10% return) in NPS Tier 1.

- You will reach ₹1.2 Cr in 30 years.

At retirement:

- 60% can be withdrawn tax-free (₹72 lakhs).

- 40% (₹48 lakhs) goes to buy an annuity, your monthly pension.

With current annuity rates (~6.5%), this ₹48 lakhs will give you around ₹25,000/month.

If you invest a lump sum in NPS ₹20,000/month in NPS, your corpus becomes ₹2.4 Cr, and now your monthly pension = ₹50,000/month.

Lump Sum vs SIP in NPS: Which is Better?

| Feature | Lump Sum Investment | SIP (Systematic Investment Plan) |

|---|---|---|

| Convenience | One-time investment in nps setup | Regular needed |

| Market Exposure | High risk during volatility | Reduced risk via averaging |

| Tax Benefit | Full benefit in one go | Spread over time |

| Ideal For | Year-end tax planners, people with surplus | Salaried individuals, regular savers |

Which One Should You Choose?

- If you’ve received a bonus, sold a property, or have idle savings, a lump sum investment in nps can be ideal.

- If you prefer disciplined investing and want to mitigate risk, SIP might suit you better.

Some investors use a hybrid approach, a lump sum to cover tax savings and SIPs for long-term wealth creation.

Weighing NPS Lump Sum vs. SIP: A Duel of Strategy

Where SIPs dance like water drops on a steady rooftop, calm, rhythmic, disciplined lump sum investments crash like a thunderstorm of capital. Each bears its unique music. Thus, a hybrid approach often strikes the golden mean. Seed your NPS with a lump sum, then nourish it monthly like a bonsai.

| Feature | Lump Sum in NPS | SIP in NPS |

|---|---|---|

| Volatility Handling | Exposed | Averaged |

| Convenience | High (once-off) | Medium (requires discipline) |

| Market Entry Risk | Higher | Lower |

| Best for | Windfalls, single-goal planning | Salary-based contributors |

Can you Withdraw Money from NPS after 5 Years?

Partial Withdrawal (before 60 years)

After 3 years of joining NPS, you can withdraw up to 25% of your funds for reasons like

- Child’s education

- Marriage

- Medical treatment

- Buying a house

You can do this 3 times in your NPS lifetime.

Exit after 5 years

- If corpus < ₹2.5 lakhs: You can withdraw the full amount.

- If > ₹2.5 lakhs: You must use 80% to buy an annuity (pension), and can only withdraw 20%.

How to Invest a Lump Sum in NPS 2025 (3 Easy Ways)

Option 1: Online via eNPS

1️⃣ Visit enps.nsdl.com

2️⃣ . Click “Subscriber Registration” → “New Registration”

3️⃣ Enter PAN, bank details, and nominee info

4️⃣ Choose Fund Manager (We recommend HDFC for consistent returns)

5️⃣ Select “Lump Sum & pay via Net Banking/UPI

Option 2: Through Your Bank

- Visit SBI, HDFC Bank, ICICI Bank (NPS Point-of-Presence)

- Submit form + KYC documents

- Deposit via cheque/DD

Option 3: Via KYC Apps like PAN eSign

- Complete the process in 15 minutes flat

My advancement from 20 Years in NPS

I’ve seen investors ignore retirement. I’ve seen them rush in without understanding. And I’ve seen the wise, the ones who planted early, waited patiently, and retired with dignity.

- Start early: one one-time investment in nps is the greatest power of NPS.

- Don’t panic in market falls: Your money is working for the long run.

- Choose the right asset mix: In your 30s, go 75% Equity. In your 50s, go balanced.

- Track once a year, not every week: Trust the system.

- Teach your children: The wisdom of NPS must be passed on.

FAQs

Can you invest ₹5 lakhs at once in NPS?

A. Yes, there is no upper limit on how much you can invest in NPS in one go.

Will I get tax benefits for a lump sum NPS?

A. Absolutely. You are eligible for deductions under Sections 80CCD(1) and 80CCD(1B), up to ₹2 lakhs in total.

Can you make multiple lump-sum payments in a year?

A. Yes, you can contribute multiple times as long as you meet the minimum per transaction and annual contribution requirements.

Is there a penalty for not contributing monthly to NPS?

A. No. As long as you contribute a minimum of ₹1,000 per year, your NPS account remains active.

Conclusion

In short, you can and should consider a lump sum investment in NPS if it aligns with your financial goals. It’s convenient, helps maximise tax benefits, and lets you lock in a potentially high-growth pension investment early. However, be mindful of the market timing and the lock-in clause.

If you’re serious about retirement planning, the NPS is an efficient, low-cost, government-backed option with long-term benefits. But like any financial decision, weigh your options and perhaps even consult a financial advisor.