You’re scrolling through mutual fund options on your investment app, and you notice two similar funds. One has a NAV of ₹15, and another shows ₹450. Your immediate thought? “The cheaper one must be a better deal, right?”

Well, hold that thought. If you’ve ever found yourself puzzled by this scenario, you’re not alone. The world of mutual fund NAVs can be surprisingly tricky, and today we’re going to unpack everything you need to know about investing in high NAV mutual funds.

Should You Invest in High NAV Mutual Funds?

What Exactly is NAV and Why Should You Care?

start with the basics. NAV, or Net Asset Value, is essentially the per-unit price of a mutual fund. Think of it like this – if a mutual fund were a pizza, NAV would be the price per slice.

But here’s where it gets interesting. Unlike that pizza analogy, a higher NAV doesn’t necessarily mean you’re paying more for the same thing. And that’s precisely where many investors get confused.

Why NAV matters in your mutual fund journey:

- It determines how many units you’ll get for your investment

- It reflects the fund’s current market value per unit

- It helps you track your investment’s performance over time

The thing is, NAV has become this mysterious number that either attracts or repels investors, often for the wrong reasons. Some folks think a high NAV means the fund is “expensive,” while others believe it signals a “premium” investment. Both perspectives miss the mark.

Breaking Down NAV: The Math Behind the Magic

Understanding how NAV is calculated isn’t rocket science, but it’s crucial for making informed decisions. Here’s the simple formula:

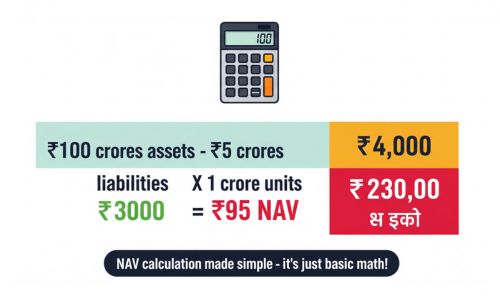

NAV = (Total Assets – Total Liabilities) / Total Outstanding Units

Let me break this down with a real example. Imagine a mutual fund has:

- Total investments worth ₹100 crores

- Cash and other assets worth ₹5 crores

- Expenses and liabilities of ₹5 crores

- 1 crore outstanding units

The NAV would be: (₹100 + ₹5 – ₹5) / 1 crore = ₹100 per unit

Here’s what drives NAV changes:

- Performance of underlying securities

- Dividend distributions

- Expense ratios

- New investments or redemptions

Now, here’s a crucial point that many investors miss: NAV alone doesn’t determine a fund’s performance potential. A fund with a NAV of ₹500 isn’t inherently better or worse than one with a NAV of ₹50. It’s like comparing a ₹500 note with five ₹100 notes – the value is the same.

Common Misconceptions That Could Cost You Money

I’ve seen too many investors make decisions based on these myths:

Myth 1: “Low NAV funds are cheaper” Reality: You get proportionally fewer units with high NAV funds, but your investment value remains the same.

Myth 2: “High NAV means the fund has performed well historically” Reality: A fund could have a high NAV due to bonus issues or simply being around longer.

Myth 3: “Low NAV funds have more growth potential” Reality: Growth potential depends on the fund’s strategy and market conditions, not its current NAV.

What to Look for When Evaluating High NAV Mutual Funds

If NAV isn’t the deciding factor, what should you focus on? Here are the key elements that actually matter:

1. Historical Performance: The Track Record That Counts

Don’t just look at absolute returns. Instead, examine:

- Consistency over different market cycles

- Risk-adjusted returns (how much risk the fund took to generate returns)

- Performance during market downturns

For instance, a fund that delivered 12% annual returns with moderate volatility might be better than one that gave 15% returns with extreme ups and downs.

2. Fund Management: The People Behind Your Money

This is where things get personal. Who’s managing your investment?

- Fund manager’s experience and track record

- Investment philosophy and strategy consistency

- Team stability (high turnover in fund management can be a red flag)

A seasoned fund manager who’s navigated multiple market cycles successfully is worth their weight in gold, regardless of the fund’s NAV.

3. Category Comparison: Apples to Apples

Always compare funds within the same category. A large-cap equity fund should be compared with other large-cap funds, not with mid-cap or debt funds.

Key metrics to compare:

- Returns over 1, 3, and 5-year periods

- Standard deviation (volatility measure)

- Sharpe ratio (risk-adjusted returns)

- Maximum drawdown during market corrections

4. Expense Ratios: The Silent Wealth Killer

This is often overlooked but incredibly important. A high expense ratio can eat into your returns significantly over time.

For equity funds, anything above 2.5% should raise eyebrows. For debt funds, keep it under 1.5%. Even a 0.5% difference in expense ratio can impact your long-term wealth creation substantially.

The Pros and Cons: Let’s Be Real About High NAV Funds

The Upside

Established Track Record: High NAV funds have typically been around longer, giving you more historical data to analyse. This longer track record can provide insights into how the fund performs across different market conditions.

Perceived Stability There’s something psychologically comforting about investing in a fund that’s been consistently growing its NAV over time. It often indicates steady, reliable management.

Less Noise from New Money Established funds with high NAVs often have a more stable investor base, which can reduce volatility caused by frequent inflows and outflows.

The Downside

Psychological Barrier Let’s be honest – it feels different buying 20 units at ₹500 each versus 200 units at ₹50 each, even though both investments are worth ₹10,000. This psychological aspect can affect your investment behaviour.

Potential for Complacency Sometimes, successful funds with high NAVs can become too large to be nimble, or fund managers might become overly conservative. This isn’t always the case, but it’s worth considering.

Higher Minimum Investment Impact. While SIPs can start from as low as ₹500, the psychological impact of seeing fewer units in your portfolio might discourage some investors from staying invested long-term.

Real-World Examples: Learning from the Market

Let me share a perspective that might surprise you. Some of the most successful mutual funds in India have very high NAVs today. Take HDFC Top 100 Fund (now HDFC Large Cap Fund) – it was launched in 1996 with a NAV of ₹10. Today, it trades at over ₹900.

Early investors who stayed invested despite the rising NAV have created substantial wealth. Those who avoided it because of “high NAV” missed out on significant returns.

On the flip side, many funds launched with ₹10 NAVs have either been merged or shut down due to poor performance. The lesson? NAV is just a number – what matters is the fund’s ability to grow your wealth.

Step 1: Clear Your Investment Goals

- What’s your investment horizon?

- What’s your risk appetite?

- Are you looking for growth or income?

Step 2: Screen Based on Performance Metrics

- Look for consistent performers over 3-5 years

- Check risk-adjusted returns

- Ensure the fund aligns with your risk profile

Step 3: Evaluate the Fund House

- Reputation and track record of the AMC

- Quality of research and fund management

- Transparency in communication

Step 4: Consider the Costs

- Compare expense ratios within the category

- Factor in exit loads if you might need early access

Step 5: Start Small and Monitor

- Begin with a small investment or SIP

- Monitor performance relative to benchmarks

- Review and rebalance periodically

The Bottom Line: Focus on What Matters

After years of observing investor behaviour and market trends, here’s what I’ve learned: successful investing isn’t about finding funds with low NAVs or avoiding high ones. It’s about finding quality funds that align with your goals and staying invested for the long term.

Remember, you’re not buying the NAV – you’re buying into the fund’s future potential to generate returns. A fund’s ability to create wealth depends on its investment strategy, management quality, market conditions, and your investment discipline.

Key takeaways for your investment journey:

- NAV is just the price per unit, not an indicator of cheapness or expensiveness

- Focus on performance, management quality, and costs rather than NAV levels

- Consistency over time matters more than short-term high returns

- Your investment horizon and goals should drive your decisions, not market noise

Your Next Steps

Should you invest in high NAV mutual funds? The answer isn’t a simple yes or no. It depends on the fund’s fundamentals, your investment goals, and your risk appetite.

Before making any investment decision, take time to research thoroughly. Use fund comparison tools, read annual reports, and if needed, consult with a qualified financial advisor who can provide personalised guidance based on your specific situation.

What’s your experience with high NAV funds? Have you avoided them in the past, or do you have success stories to share? The mutual fund journey is deeply personal, and everyone’s path to wealth creation is unique.

Remember, the best time to start investing was yesterday. The second-best time is today. Whether the fund has a NAV of ₹15 or ₹1,500, what matters is that you begin your wealth creation journey with the right knowledge and mindset.

Share your frinds and more intersting and informative blog post see moneykoan

Disclaimer: This article is for educational purposes only and should not be considered as investment advice. Please consult with a qualified financial advisor before making investment decisions. Mutual fund investments are subject to market risks.